Ontarians on the Move, 2021 Edition. The Short Version

My Ontarians on the Move series is fairly lengthy, so here’s the short version for busy people.

TL;DR version: Ontario’s population grew by one million people in the last five years, after growing by less than 600,000 in the previous five. This unanticipated surge caused a shortage of family housing, starting in the Toronto market and radiating across the province thanks to drive until you qualify and the musical chairs effect. House prices skyrocketed across the province and an influx of young families breathed new life into many smaller communities. Then COVID happened, things got really weird, and gasoline was thrown onto the house-price fire.

In the last five years, Ontario’s population grew by over one million people. The five years prior, it grew by less than 600,000.

The province did not anticipate this level of growth. Government forecasts from 2015 had anticipated population growth of closer to 700,000 people over five years. Population growth in 2017, 2018, and 2019 each exceeded the most optimistic of government forecasts.

This unanticipated population growth fundamentally altered how and where Ontarians work and live.

Why did Ontario’s population grow faster than in the past?

There were two big sources:

Ontario saw an increase in the level of immigration due to a combination of an increase in immigration targets (first from Harper, then from Trudeau) and the oil price plunge making Alberta a relatively less attractive destination than Ontario.

The biggest change was in the number of non-permanent residents, primarily (but not exclusively) due to an international student boom at our colleges and universities.

These two sources of new Ontarians were disproportionately young, with the net non-permanent population primarily comprising of people between the ages of 17–24, and the new immigrant population largely made of people in their late 20s and early 30s. When we consider that a lot of these new Ontarians started out as international students in the province, this makes a great deal of sense. Bright young students move to Ontario at age 18 or 19, go to college or university, work for a year or two on a visa, and obtain Canadian citizenship in their late 20s.

In total, we saw an additional 500,000 people, between the ages of 16 and 31, moving to Ontario in just five years.

The combination of an influx of young internationals and an aging population has substantially altered the province’s age profile. We have a lot more people in their 70s, thanks to the aging of the baby boomers, and a much larger population of 20-somethings.

This helps explain the boom in 1- and 2-bedroom apartments and condos over the past five years; these property types are particularly popular with those age segments.

It has also caused an increase in the demand for family-sized housing. This demand is radiating outward from Toronto and being felt across the province.

It all begins in Toronto

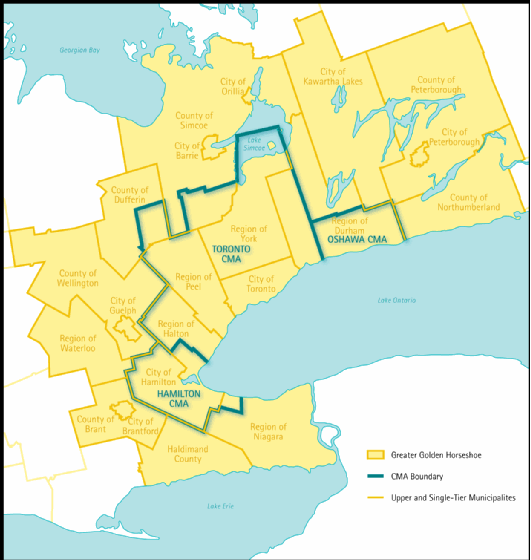

In order to understand what’s happening to population growth and home prices in London or Peterborough, we have to start from Toronto.

Specifically, we’ll look at Toronto CMA (Census Metropolitan Area), as shown below:

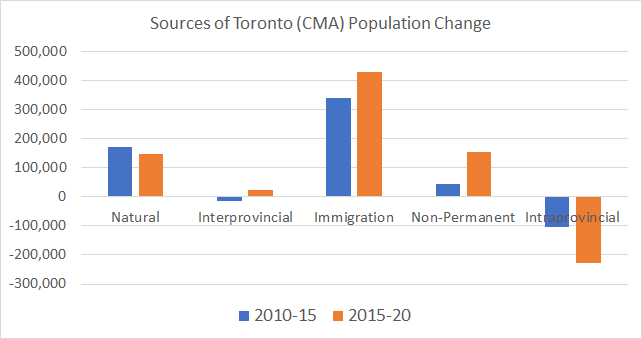

Over the past five years, 53% of net new non-permanent residents have settled in Toronto CMA, along with over 80% of net new immigrants. It’s also seen an outflow of 227,400 people to other parts of the province (intraprovincial migration), over double the level from the previous five years:

In 2010–15, the number of non-permanent residents and immigrants in metro Toronto rose by 385,000. Growth accelerated in the 2nd half of the decade, with an additional 583,000 non-permanent residents and immigrants calling metro Toronto home, a 50% increase.

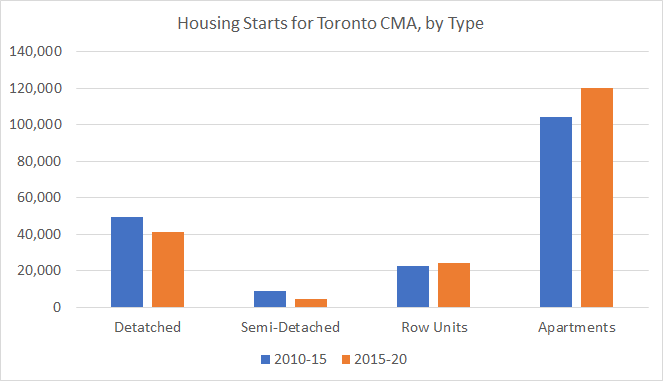

You would think if the population growth rate from international sources grew by 50% metro Toronto would increase their rate of new residential construction by about 50%. For every 2 houses, apartment units, and condos we were building before, we now should be building 3.

What actually happened was… not that. Here is the data on new housing starts for Toronto CMA:

Apartment construction rose by 15%, but this was offset by a near-collapse in the building of semi-detached units. The building of detached housing, dropped by 17%.

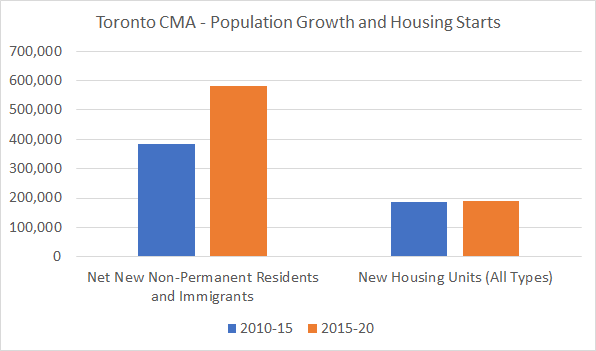

Construction of total new units in metro Toronto rose by only 3%, an increase of just over 5000. 5000 extra units to house 200,000 more people; that’s 40 people per unit. And those extra units were apartments; the growth in detached, semi-detached, and row homes fell by over 10,000. The growth rate in the number of bedrooms constructed in metro Toronto likely fell over the last five years, while population growth from non-permanent residents and immigration increased by 200,000.

People left Toronto because they had to leave Toronto. There simply were not enough places for everybody to live, as residential construction (of any type) was not keeping up with population growth. And people are continuing to leave metro Toronto.

Some of the people leaving Toronto CMA are older residents looking to “cash-out” on high real-estate prices, but the most common group are young families. The top-10 most common ages to leave Toronto are the ten between the ages of 31–35 and 0–4. The single most common age is zero — that is, babies under the age of 1. That’s who is leaving Toronto.

Where are they going to? We have three years' worth of point-to-point intraprovincial migration data, from 2016–19. Not surprisingly, they are moving to nearby CMAs:

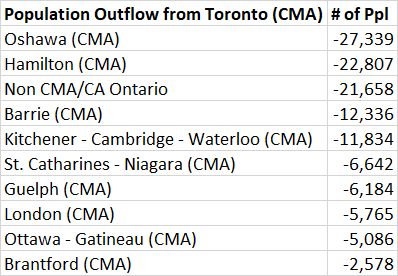

Typically, these young families are still working in Toronto, but moving to a community where they can afford to buy a place large enough to suit their families. This is a process known as drive until you qualify. That is, get in the car, and drive far enough away that the home prices are low enough that a bank is willing to qualify you for a mortgage that’s large enough to buy the house. Some are able to move to the neighbouring CMAs of Hamilton and Oshawa. Others are having to drive until they qualify to places further afield like London and St. Catharines.

Drive Until You Qualify and the Musical Chairs Effect

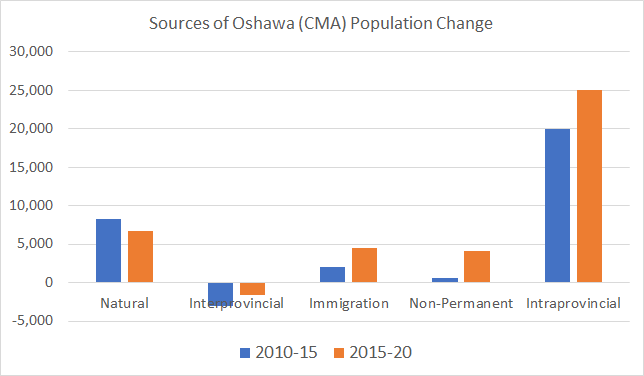

Next let’s consider Oshawa CMA, which is growing almost entirely due to an influx of residents from other parts of the province:

Though it’s unnecessarily vague to suggest that Oshawa is gaining residents from “other parts of the province” — the influx is coming from exactly one place. Toronto. However, Oshawa is also losing a lot of residents to other parts of the province in the three years in which we have data.

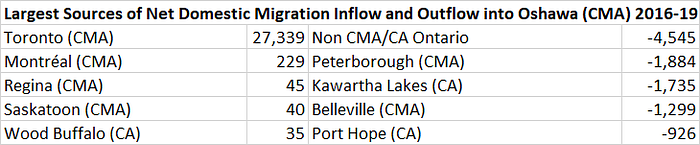

Oshawa is losing population, on net, to rural Ontario (show here as Non CMA/CA Ontario) as well as to Peterborough, Kawartha Lakes, and Belleville.

Drive until you qualify (among other factors) is causing an influx of residents to Oshawa. This drives up house prices in Oshawa, which can price out local residents wanting to buy housing, causing them to move to less expensive markets like Peterborough and Belleville, where they often commute back to their jobs in Oshawa (or Toronto). This musical chairs effect is pushing families, like ripples in a pond, into new communities across the province. Barrie CMA is gaining people from Toronto, but losing them to Midland and Orillia:

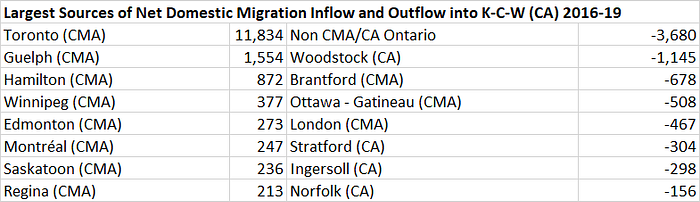

Kitchener-Cambridge-Waterloo is gaining people from Toronto, in part thanks to lower real estate prices and in part due to a booming tech sector. This is pricing many residents out of the local market, and causing them to move to smaller, less expensive markets like Woodstock, Stratford, and Ingersoll, which is causing those markets to rapidly appreciate:

The path of musical chairs can get quite complex. Toronto residents moving to Kitchener, Kitchener residents moving to Brantford, Brantford residents moving to Norfolk and Woodstock, and real-estate prices going up everywhere along the way:

And we should keep in mind, this point-to-point migration data only extends to July 2019 — all of this was happening pre-COVID.

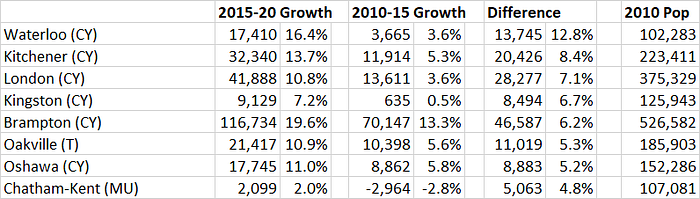

At the municipal (rather than metro) level, this has caused a big increase in the growth rates of larger communities, such as Kitchener, Waterloo, London, and caused shrinking communities like Chatham-Kent to return to growth:

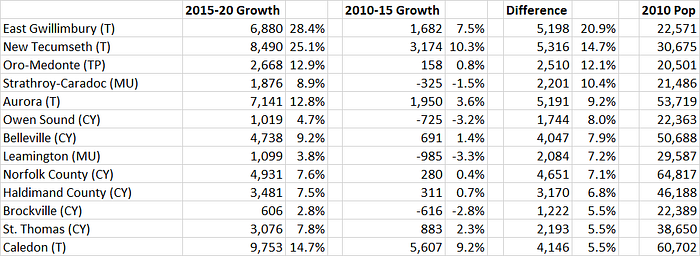

Communities with populations between 20,000 and 100,000 are also seeing big jumps in their growth rates, such as St. Thomas and Strathroy-Caradoc, popular destinations for families that have been priced out of the London market:

Summarizing the pre-COVID Ontarians on the Move story

This unanticipated population increase caused home price escalation in most of the province, as there were more families chasing housing than the number of available properties. People having to drive until they qualify and the musical chairs effect pushed families further away from where they work, increasing commute times and putting additional strain on our transportation infrastructure. It also caused some communities, that had stable or even declining populations to experience growth again, due to an influx of young families.

How has COVID changed things?

A lot of things have changed during the pandemic. There are six megatrends that I believe are relevant to the Ontarians on the Move story:

- A slowdown in the growth of international students and people on work visas in the province.

- A collapse of the tourism market.

- A huge increase in the savings-rate of white-collar professionals due to a collapse in spending.

- A big increase in work-from-home

- A big increase in shop-from-home

- Global interest rates falling to near zero (and in some cases, below zero).

The first two trends have taken some of the pressure off of the rental market. The demand for those properties is not as high as we would have predicted pre-COVID, and a collapse in tourism has caused some properties used for Airbnb to flow back into the rental stock.

The final four megatrends have thrown gasoline on regional housing markets. White-collar professionals have found themselves with a lot more money, which is flowing into everything from stocks to retro games to hockey cards. That increase in savings is allowing home buyers to make even larger downpayments and increase the size of their offers.

Work-from-home and shop-from-home lowers the cost of living further away from your job and your favourite stores, since your job and your favourite stores are now on the laptop in your home office. If you were thinking of living in Woodstock before, you might have hesitated because it’s a long commute to your job in Toronto and it’s far away from an Ikea. But now we’re not going to our jobs in Toronto and Ikea’s been closed half the time anyway, Woodstock is a whole lot more attractive.

And, finally, interest rates, including mortgage rates, have fallen sharply. If we think in terms of monthly payments, a $900,000 mortgage now has a lower monthly payment than a $600,000 one would have had two years ago, allowing families to make much larger offers than they did two years ago (at the risk of a rate shock when that mortgage rolls over five years from now).

Side note: I renewed my mortgage two years ago. Yes, I have some regrets.

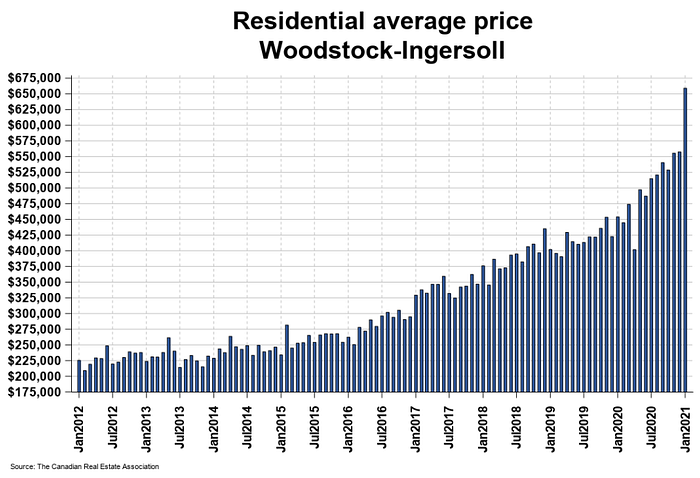

This has caused real-estate markets like Woodstock-Ingersoll, which were already hot pre-COVID, to absolutely explode:

Most of Canada’s hottest real-estate markets are currently in Ontario:

The largest y-o-y gains — above 30% — were recorded in the Lakelands region of Ontario cottage country, Northumberland Hills, Quinte & District, Tillsonburg District and Woodstock-Ingersoll.

Y-o-y price increases in the 25–30% range were seen in Barrie, Niagara, Grey-Bruce Owen Sound, Huron Perth, Kawartha Lakes, London & St. Thomas, North Bay, Simcoe & District and Southern Georgian Bay.

This was followed by y-o-y price gains in the range of 20–25% in Hamilton, Guelph, Oakville-Milton, Bancroft and Area, Brantford, Cambridge, Kitchener-Waterloo, Peterborough and the Kawarthas, Ottawa and Greater Moncton.

What will things look like post-COVID

It depends on what happens to our six mega-trends:

- A slowdown in the growth of international students and people on work visas in the province.

- A collapse of the tourism market.

- A huge increase in the savings-rate of white-collar professionals due to a collapse in spending.

- A big increase in work-from-home

- A big increase in shop-from-home

- Global interest rates falling to near zero (and in some cases, below zero).

It is straight-forward to make both bearish and bullish cases for non-Toronto real-estate markets.

The bearish case is that if (or as most people say when. I say if) interest rates rise substantially and saving rates return back to traditional levels, the ability of families to make large offers will fall, and house prices will return to something resembling their pre-COVID levels.

The bullish case is that work-from-home will persist, making markets like Woodstock continue to be attractive, which will continue to put upward pressure on prices.

But over the next five-to-ten years, I’d put population growth, particularly the growth of non-permanent residents, as the primary driving factor. If Ontario continues to be an attractive destination for international talent, expect these pressures to continue. On the other hand, if students and workers become less interested in the province (perhaps due to the Biden immigration reforms), then the drive until you qualify and musical chairs effect, that were so prominent in 2015–2020, will be substantially diminished for the rest of the decade.