Basic Income: What federal income supports could be folded into one?

Yes, it’s another Basic Income piece! *sigh*

TL;DR: Want to hobble together a Basic Income out of existing federal income supports, but don’t want to touch targeted programs for disabilities or medical expenses? Turns out, there’s not much left, beyond the Basic Personal Amount and the GST credit. But that is a starting point, and those could be reformed. In short, the notion that there are a plethora of different federal cash supports is a myth.

In response to yesterday’s piece on how the PBO’s Basic Income model would impoverish single mothers, two different parliamentarians reached out to me with thoughtful emails. Their thinking is that a federal Basic Income should leave disability, medical, and caregiver programs alone, and that the federal government cannot eliminate provincial programs. Instead, a basic income would simply fold in existing non-targeted income supports.

This is an idea I could get behind, though my philosophy is to figure out what problem you want to solve first, then design the best policy for the job, rather than start with the policy and determine what problem it might solve.

One issue that will crop up with a “fold it in” strategy that recognizes federalism and leaves disability supports intact: there’s not a lot to fold in. Let’s go back to our list of all the credits that the PBO report folded into the Basic Income proposal they analyzed.

Next, let’s remove anything that is in provincial jurisdiction, along with any federal credit that involves disability, medical, or caregiving support. I’ll mark the provincial programs in blue, and the federal programs we’d like to leave untouched in red.

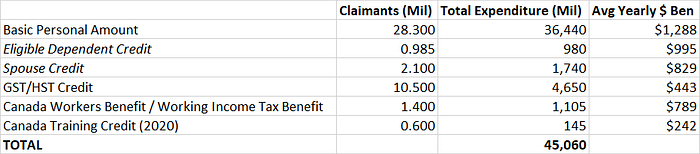

Here are the details on the four remaining programs on our list:

This reduces the income tax bill of Canadians:

Individual taxpayers can claim a non-refundable credit in respect of the Basic Personal Amount. The value of the credit is calculated by applying the lowest personal income tax rate (15% in 2020) to the Basic Personal Amount. The credit amount is indexed to inflation… In December 2019, the Government announced its intention to increase the Basic Personal Amount to $15,000 by 2023. The increase will be gradually implemented from 2020 to 2023 through annual increases in excess of inflation. The new, increased portion of the credit will be subject to an income test beginning at a level of individual net income equal to the fourth federal tax bracket threshold ($150,473 in 2020), and be fully phased out by the fifth federal bracket threshold ($214,368 in 2020).

Built into the BPA is the Spouse or Common-Law Partner Credit which allows a spouse to claim the BPA on behalf of a spouse who isn’t using it (since they don’t earn enough income) and the Eligible Dependant Credit (EDC) which allows single individuals to claim an additional BPA on behalf of a child or dependent family member. The loss of the EDC under the PBO Basic Income plan is what would make it such a disaster for low-to-middle income single parents, should it ever become law.

It’s important to note that the BPA is a non-refundable tax credit, meaning that it can only be applied against income tax owing. As such, not everyone receives the maximum value of the BPA. The BPA is incorporated into the taxes you remit each pay period, so it’s about the only credit where you don’t necessarily have to file a tax return to receive the value from it.

This helps workers offset the costs of training programs:

Introduced in Budget 2019… Qualifying workers between the ages of 25 and 64 will accumulate a credit balance of $250 per year, up to a lifetime limit of $5,000. The credit balance can then be used to refund up to half the costs of taking a qualifying course or training program. In order to accumulate a Canada Training Credit balance in 2020, a worker must have earnings of $10,100 or more (including maternity or parental leave benefits) and must have net income below the upper limit of the third federal tax bracket ($150,473 in 2020).

Treating this as an income-support program is a stretch, but for completeness, I left it on here.

Goods and Services Tax/Harmonized Sales Tax Credit

This compensates low-to-middle income individuals and families for the GST/HST they pay:

A refundable income tax credit (now known as the GST/HST Credit) was established at the time of the introduction of the GST to ensure that low-income families would be better off under the new sales tax regime than under the former federal sales tax. The amount of the credit depends on family composition and income. Specifically, for the period from July 2020 to June 2021, based on net family income reported for the 2019 taxation year:

an adult receives a basic adult credit of $296 per year;

families with children aged 18 and under receive a basic child credit of $155 per year for each child;

single parents can claim, in lieu of the basic child credit, the full basic adult credit of $296 per year for one dependent child;

single parents are eligible for an additional credit of $155 per year in addition to their basic credit, child credits and full basic adult credit for the first dependent child; and

single adults without children are eligible for an additional credit of up to $155 per year (depending on income) in addition to their basic credit.

The value of the credit is reduced for individuals and families with annual incomes over $38,507. Both the credit amounts and the income threshold are adjusted annually for inflation.

This credit is substantially different than the Basic Personal Amount in four ways:

- It’s refundable — your income cannot be too low such that you do not receive it.

- You need to file a tax return in order to receive it, unlike the BPA which can be (imperfectly) incorporated into the cheques you get each pay period. This is important, as roughly 15% of Canadians do not file a tax return and essentially fall through the cracks when it comes to these programs (including 97% of all people experiencing homelessness).

- The value of the credit is phased out at much lower income levels than the BPA.

- The GST/HST credit is paid out four times per year, whereas the BPA is incorporated into the amount deducted from your paycheque each pay period (and then reconciled when a tax-return is filed).

And finally, we have the (old) Working Income Tax Benefit

Canada Workers Benefit / Working Income Tax Benefit

This is a program designed to boost the after-tax income of lower-income workers, with an added emphasis on workers with a disability:

The Canada Workers Benefit (CWB) is a refundable tax credit that supplements the earnings of low-income workers. It is generally available to individuals 19 years of age and older not attending school full-time. The refundable credit is equal to 26% of each dollar of earned income in excess of $3,000 to a maximum credit of $1,381 for single individuals without dependants and $2,379 for families (couples and single parents) in 2020. The CWB is phased out at a rate of 12% of each dollar of adjusted net income above thresholds of $13,064 for single individuals without dependants and $17,348 for families in 2020. An additional CWB supplement of up to $713 in 2020 is provided to persons eligible for both the CWB and the Disability Tax Credit. The CWB supplement is phased out at a rate of 12% of each dollar of adjusted net income above a threshold of $24,569 for single individuals without dependants and $37,176 for families in 2020.

It is a form of income support, but one designed to help get (and keep) people in the workforce.

How could we combine all four?

As you’ve probably guessed by now, it would be tricky to combine all four of these programs into a single-income support. They have very different features (refundable vs. non-refundable), target different populations (the general public vs. low-to-middle income Canadians vs. workers) and are paid out at different times.

But let’s suppose we really wanted to do it. Who gets these benefits now, and what’s the total amount of money in the pot? Fortunately, the Report on Federal Tax Expenditures has us covered. I’ll use 2018 tax year data for the analysis (due to stronger data quality) except for the Canada Training Credit, which didn’t exist in 2018, so we’ll use a 2020 projection.

Here’s the data, showing the number of claimants, the total government expenditure (in millions) and the average yearly benefit per claimant:

A full 87% of the total expenditure of these programs comes from the Basic Personal Amount (and associated Eligible Dependent and Spouse credits). Given the relatively modest expenditure of the other programs, relative to the BPA, and how they serve different purposes (and are paid out at different times), that’s a relatively large change for a rather modest gain.

Without adding a whole lot more money to these programs, it’s hard to see a winning formula here (and many have tried). You could keep the BPA intact, and fold the other programs in. You’d have something that (very roughly) looks like this:

The average yearly benefit of the BPA has now gone up by about 300 dollars a year, but since the GST/HST and CWB/WITB credits target lower incomes, this is an income transfer to lower to higher-income individuals.

You could go the other way, and have a combined program that has a phase-out that looks more like the GST/HST credit. That would (very roughly) look something like this:

That’s far more progressive, with an average yearly pay-out, per recipient of $4,291. But the number of overall recipients has fallen by almost 18 million Canadians! A middle-income couple would not qualify for this benefit and simulataneously lose both of their BPAs, which combined are worth $4,000 a year.

A $4,000 tax hike on middle-class families feels like a political non-starter.

In short, for this to work, you’d have to increase funding to this, and by an awful lot. And then it’s the added funding that’s doing the heavy lifting, not the fact that you’ve tried to combine a bunch of programs that serve very different purposes together.

I really don’t understand the point of this approach. As before, I’d suggest starting from a problem-based perspective; let’s figure out what we’re trying to do, then solve it.

But if we’re absolutely committed to altering these programs, and we’re committed to spending some money (of course, that raises the question of where that money would come from), there’s a far-simpler, far-more straightforward two-part solution. Here it is:

- Make the BPA refundable, so low-income individuals receive the full benefits of it. My back-of-the-envelope estimate (along with this paper from Simpson and Stevens) is that the yearly cost would be in the $20–25 billion a year range.

- Introduce automatic filing of tax returns, along with an initiative to get the most marginal and vulnerable Canadians known to the tax system, so they can collect all the benefits to which they’re entitled.

Not nearly as sexy as developing an exciting new policy from scratch, but it would be far simpler and more effective.